Japan's Crypto Tax System in 2026 — What Global Investors Should Know

Japan's approach to cryptocurrency taxation has quietly evolved into one of Asia's most sophisticated frameworks—and it's about to shift again in 2026. For global investors holding Japanese exchanges like GMO Coin or Liquid, or Japanese residents managing international portfolios, understanding these rules isn't optional. The difference between proper reporting and penalties can easily exceed six figures in JPY, even for mid-sized traders.

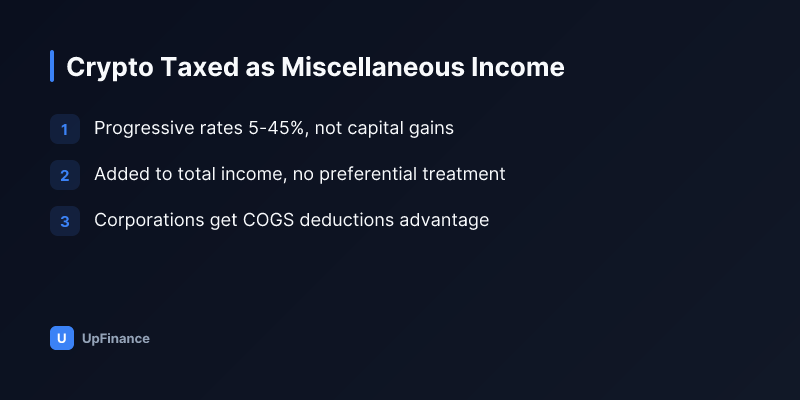

Unlike the US, which treats crypto as property under capital gains rules, or the EU's emerging patchwork of VAT and income classifications, Japan has settled on a clearer (if stricter) model: cryptocurrency gains are treated as miscellaneous income taxed at progressive rates, with no preferential capital gains treatment. That structure is holding firm into 2026, but important details around staking rewards, cross-chain swaps, and foreign exchange reporting have tightened.

This guide walks you through what's changed, what hasn't, and how it affects both Japan-based traders and foreign investors with Japanese tax obligations.

Japan's Crypto Tax Classification: The Fundamentals

Japan's National Tax Agency (NTA) settled its classification framework in 2017-2018 and has held steady since. Cryptocurrency gains are taxed as "miscellaneous income" (雑所得, zatsu shotoku) at progressive ordinary income tax rates—not capital gains rates.

What does this mean in practice?

- Individual resident traders: Combined income from crypto is added to your salary, business income, and other sources. Your marginal tax rate applies, ranging from 5% to 45% depending on your total income bracket (plus a 2.1% reconstruction tax through 2037).

- Non-resident foreigners: If you're a foreign investor with Japanese-source crypto income, you're generally not subject to Japanese income tax unless you engage in regular, habitual trading that constitutes a "business." One-off trades or long-term holdings usually escape Japanese tax.

- Corporations: Japanese entities treating crypto as business inventory can deduct cost-of-goods-sold (COGS) and operating expenses. This has made corporate crypto trading more tax-efficient than individual trading.

This is fundamentally different from the US Section 1231 treatment, where long-term capital gains receive preferential 15-20% rates. A Japanese trader realizing 50 million JPY in gains faces marginal rates around 40-45%, not 20%. This structural difference is why many international crypto hedge funds operating in Asia have chosen to incorporate their Japanese operations as tax-resident companies rather than individual partnerships.

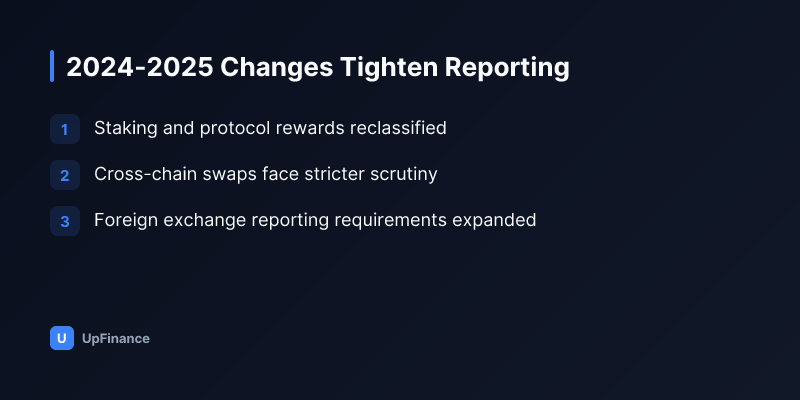

What Changed in 2024-2025, and What's New for 2026

The NTA clarified several rulings between 2024 and early 2026 that tighten reporting and alter how certain transactions are classified.

Staking and Protocol Income

Previously, the treatment of staking rewards was ambiguous. As of 2026, staking income is classified as miscellaneous income at fair market value on the date received, not the date sold. This applies to:

- Proof-of-Stake (PoS) validator rewards (e.g., Ethereum staking)

- Liquid staking token rewards (e.g., Lido's stETH airdrops in Japan)

- DeFi yield farming rewards

A critical implication: if you stake 10 ETH worth 3 million JPY and receive 0.5 ETH as annual rewards, you owe tax on the reward's JPY value on the distribution date—not later when you sell that reward.

This creates a timing mismatch. Many Japanese DeFi participants now use tax-deferral strategies like:

- Staking in foreign exchanges or Layer 2 solutions before repatriating

- Holding rewards in separate wallets to clearly track cost basis

- Using UpFinance's AI tax tracking tool (if operating in Japan) to auto-flag reward dates

Hard Forks and Airdrops

Hard forks (new coin issuances) and unexpected airdrops have been taxable events in Japan since 2019, but enforcement was spotty. The 2026 NTA guidance tightened the definition: any unsolicited receipt of new tokens triggers income tax on fair market value at receipt date.

Examples:

- Bitcoin Cash fork from Bitcoin: taxable in 2017 for Japanese holders

- Ethereum Shanghai upgrade staking rewards: taxable on receipt

- Random airdrop campaigns (e.g., Arbitrum's ARB airdrop in 2023): taxable

Foreign investors (non-Japanese residents) generally avoid this, but Japanese residents can't.

Cross-Chain Bridges and Swaps

Decentralized Finance (DeFi) participants moving assets across chains using bridges (Stargate, LayerZero, Synapse) now face clearer guidance: each bridge transaction is treated as a disposal and repurchase, triggering capital gains or loss realization.

This is significant. A trader moving 100 USDC from Ethereum to Arbitrum is, from the NTA's perspective, selling USDC at Ethereum fair market value and buying USDC at Arbitrum fair market value. If there's a slippage or fee differential, a taxable loss or gain crystallizes.

Tax Rates and Brackets for 2026

Japanese income tax is fully progressive. Your crypto gains are added to your total income for the year, and you pay tax at marginal rates:

| Total Annual Income (JPY) | Tax Rate | Includes Reconstruction Tax |

|---|---|---|

| 0 – 1,950,000 | 5% | 5.105% |

| 1,950,001 – 3,300,000 | 10% | 10.21% |

| 3,300,001 – 6,950,000 | 20% | 20.42% |

| 6,950,001 – 9,000,000 | 23% | 23.483% |

| 9,000,001 – 18,000,000 | 33% | 33.693% |

| 18,000,001+ | 45% | 45.945% |

Additionally, residents are subject to local inhabitant tax (住民税) at approximately 10%, applied separately to the same income base.

Combined top rate for Japanese residents: ~55.945% (45% national + 10% local + 0.945% reconstruction).

For context, this exceeds the top US federal capital gains rate (20%) and aligns more closely with EU member states like Denmark (55.9%) or Spain (47%).

Deductions and Loss Carry-Forward

One advantage Japan offers is broad deduction eligibility:

- Trading expenses (exchange fees, hardware wallets, educational materials, VPN/security software)

- Professional advice fees (tax consultants, auditors)

- Home office allocation (if crypto trading is your primary business)

- Losses can be carried forward indefinitely in the same income category

However, losses in miscellaneous income cannot offset capital gains from stock trading or real estate sales—a major constraint. Losses are siloed within the miscellaneous income bucket.

Reporting Requirements and Compliance

Who Must Report?

Any individual resident in Japan with crypto gains exceeding approximately 200,000 JPY must file a supplementary tax return (修正申告, shusei shinkoku). You may also need to report if:

- You realized any capital losses you wish to carry forward

- You received staking rewards or airdrops above 50,000 JPY

- You actively traded on Japanese exchanges (reporting by the exchange to NTA is automatic)

Non-residents who are not Japanese citizens or residents generally don't file, but if you held assets in a Japanese exchange account, the exchange reports to authorities—transparency is high.

Documentation Standards

The NTA expects detailed records:

- Transaction log: Date, asset, quantity, JPY equivalent (using daily average rates from publicly available sources)

- Cost basis: Original acquisition date, amount in JPY, source (purchase, fork, airdrop, staking)

- Exchange records: Statements from all platforms used

- Proof of reporting: Screenshots of exchange confirmations

Most Japanese tax software (e.g., Freee, MFCloud) now integrates crypto exchange APIs, auto-importing transactions. For international traders using Coinbase, Kraken, or Binance, you'll need to manually export CSV data or use third-party aggregators that support Japanese tax reporting.

Planning Strategies for Global Investors

Strategy 1: Residency and Structure

If you're a high-income crypto trader, tax residency matters enormously. A trader with 500 million JPY in gains faces:

- Japanese resident: ~280 million JPY in taxes (55.945% combined rate)

- Non-resident in Singapore or UAE: ~0-5% in taxes (or deferred), plus logistics cost (~500k JPY)

Many mid-to-large crypto funds have established Singapore or Hong Kong entities to manage Asia exposure, routing Japanese trades through these entities. This is legal and widely used.

Strategy 2: Timing Gains and Losses

Since Japan allows loss carry-forward indefinitely (unlike the US 3-year limit), strategic harvesting is viable:

- Realize losses in volatile years to offset future gains

- Defer staking rewards to the following calendar year when possible

- Batch large trades to minimize realization across multiple tax years

This requires discipline but can save 100k+ JPY across a multi-year cycle.

Strategy 3: Use Corporate Structure for Serious Trading

A Japanese corporation trading crypto can deduct business expenses, pay corporate tax at ~30% (national + local), and dividend remaining profits at preferential rates if taken as salary. This is especially effective for traders with >100 million JPY annual turnover.

Drawbacks: More accounting overhead, corporate filing requirements, and minimum 2% corporate local tax even with zero profit.

Strategy 4: Staking in Sheltered Jurisdictions

If you're a non-resident with Japanese assets, staking through non-Japanese platforms (Lido, Rocket Pool) before repatriating avoids the Japanese staking-receipt-date rule. This is an edge used by sophisticated investors but requires careful documentation to show non-Japanese sourcing.

The Broader Context: Japan vs. US and EU

| Factor | Japan | USA | EU (varies) |

|---|---|---|---|

| Tax Classification | Miscellaneous income (no preferential rate) | Capital gains (15-20% long-term) | Property or income (varies) |

| Top Rate | 55.945% individual | 37% (federal) + 3.8% NIIT | 47% (Spain) to 55.9% (Denmark) |

| Staking Income | Taxable at receipt (JPY fair value) | Taxable at receipt (USD fair value) | Taxable (France: 45%) |

| Loss Carryback | No | No (carryforward 3 years) | No (varies by member state) |

| Foreign Tax Credit | Available for foreign taxes paid | Available | Available (EU citizens) |

| Reporting Ease | Software integrations available | IRS Form 8949, Schedule D | No standard form (national rules) |

Japan's system is not inherently worse, but it penalizes high-income traders more than the US or Singapore. However, Japan's clarity and consistent enforcement since 2017 make it easier to plan than, say, the EU's fragmented approach.

Looking Ahead: 2026 and Beyond

The NTA has signaled no major legislative changes for 2026, but regulatory focus is intensifying on:

- Decentralized Finance (DeFi) income sourcing: How to attribute income to non-custodial protocols

- NFT and metaverse asset taxation: Clarity expected by late 2026

- Cross-border reporting: Alignment with OECD Common Reporting Standard (CRS) data exchanges

Expect heightened enforcement on Japanese residents trading on foreign exchanges—data sharing between Japan's Financial Services Agency (FSA) and overseas regulators is accelerating.

Practical Next Steps

If you're a global investor with Japanese tax exposure, consider:

- Audit your cost basis: Gather all transaction records dating back to your first purchase. Even rough estimates are better than missing data.

- Consult a local CPA: A Japanese tax professional (税理士, zeirisishi) costs ~500k–1 million JPY annually but can identify deductions and structures you'd miss.

- Use UpFinance or similar tracking tools: Auto-categorizing transactions by tax type (staking vs. trading) saves hours during tax season.

- Evaluate structural changes: If your annual crypto income exceeds 50 million JPY, consider incorporating or relocating residency.

- Document everything: Especially for cross-chain transactions, DeFi yields, and airdrop dates.

The cost of non-compliance—penalties, interest, and audits—dwarfs the cost of professional planning. Japan's NTA is increasingly aggressive on high-income cases, and offshore accounts offer no shield.

This content is produced for marketing purposes by MIG Korea Group and is not investment advice. Crypto investing carries the risk of losing your principal; investment decisions are your own responsibility. UpFinance is the AI fintech service of MIG Korea Group.

Related posts

Start AI investing with UpFinance — free

Start free →Smart investing with UpFinance

AI-powered market analysis, automated portfolio rebalancing, and risk alerts.

We make crypto markets simple — without dumbing them down.