Why Gen Z Investing Strategies Diverge Wildly Across Korea, Japan, and the West

The Divergence: How Gen Z Money Moves Differently by Geography

If you're watching global fintech, you've probably noticed something odd: Gen Z (born 1997-2012) invests in radically different ways depending on which side of the world they live on. A twenty-five-year-old in Seoul might have forty percent of their portfolio in mid-cap altcoins and leverage trading, while their peer in Tokyo spreads risk across regulated mutual funds and index funds, and a New Yorker in the same cohort is divided between fractional stock apps and a Roth IRA.

This isn't coincidence—it's the result of regulation, culture, inflation expectations, and which fintech platforms reached critical mass first.

The story is especially sharp in Asia, where two of the world's largest developed economies have taken almost opposite regulatory approaches to retail trading and cryptocurrency. Korea has embraced retail crypto with light-touch oversight that has created one of the most liquid and sophisticated retail trading markets on Earth. Japan, by contrast, learned harsh lessons from the Mt. Gox collapse and has implemented strict licensing regimes that make it harder (but safer) for young investors to access speculative assets. And the West sits somewhere in between—fragmented by jurisdiction, but broadly moving toward stricter custody rules and investor protection frameworks.

Understanding these differences matters because Gen Z's investment choices today will shape global capital flows for the next three decades. If you're building fintech products, managing institutional capital, or even just trying to understand where the next bull market signals might emerge, you need to know why Korean retail investors trade differently from their Japanese and Western counterparts.

The Korean Model: Velocity, Leverage, and Regulatory Arbitrage

Let's start with the most aggressive market: South Korea.

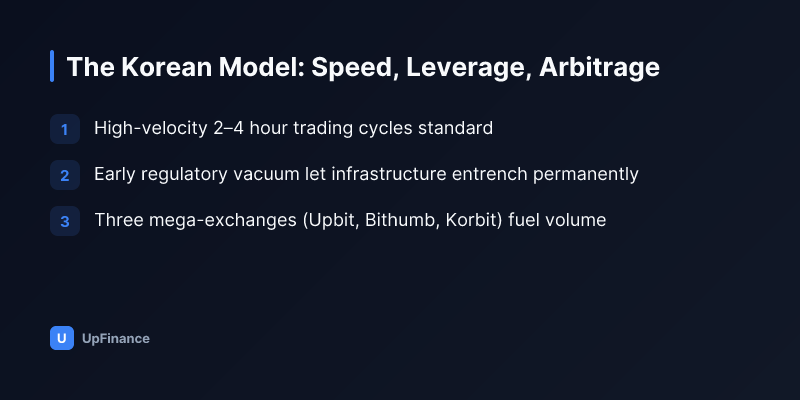

Korean Gen Z investors have become synonymous with high-velocity, high-conviction trading. Walk into any PC bang (internet café) in Gangnam, and you'll see teenagers and twenty-somethings watching four-monitor setups tracking Upbit, Bithumb, and Korbit—the three largest Korean crypto exchanges. They're not buy-and-hold investors. They're trading on 2–4 hour cycles, using leverage, and treating Korean-won-denominated spot and futures markets as their native asset class.

Why Korea Became the Crypto Retail Trading Capital

Korea's path to crypto dominance came from three factors:

-

Regulatory vacuum filled by early adopters: When Bitcoin arrived in Korea around 2009-2010, there was no regulatory framework. By the time regulators caught up (around 2017-2018), the infrastructure—exchanges, communities, media—was already entrenched. The government implemented anti-money-laundering (AML) rules and real-name verification, but it never banned crypto or futures trading the way China did.

-

Inflation fear and currency devaluation anxiety: The Korean Won has been under structural pressure for years due to demographic decline and capital outflows. Younger Koreans, who remember the 1998 Asian financial crisis through family stories, are skeptical of holding assets denominated purely in KRW. Crypto offered an alternative store of value and a hedge against currency risk.

-

Mobile-first fintech infrastructure: Korea has the world's fastest internet (average 28 Mbps), and the population adopted mobile banking in the early 2000s—before the US. By the time crypto exchanges emerged, Koreans already had the habit of managing money on phones. Apps like Upbit (owned by Dunamu) integrated seamlessly into the existing fintech ecosystem.

"Korean Gen Z doesn't see crypto as an investment class separate from stocks or forex. It's just another asset on their phone, with better volatility and lower fees than traditional brokers." — Regional fintech analyst, Seoul, 2025.

The Leverage Culture

One of the most distinctive features of Korean retail trading is the normalization of leverage. Korean crypto exchanges offer spot trading with margin up to 5x, and futures contracts with up to 125x leverage on some pairs. This is not uncommon for a Korean investor in their twenties to maintain a 2-3x leveraged position in altcoins as part of their regular portfolio.

Why? Because the volatility is there to exploit, and because Korean traders have access to real-time orderbook data, low fees, and community knowledge that makes leverage feel manageable. Korean trading communities on Naver Cafe, YouTube, and Telegram maintain detailed technical analysis, share leverage signals, and collectively track on-chain metrics in ways that Western retail communities do not.

However, leverage comes with liquidation risk, and every bull market in crypto sees Korean retail traders wipeouts. This is culturally accepted as part of the game—a rite of passage—rather than a warning sign that the market is too risky.

Government Regulation and the Real-Name Account Rule

In 2021, South Korea passed the "Real Name Account Rule," which required all crypto exchange deposits to come from bank accounts registered to the trader's real name. The intent was AML compliance, but the effect was to legitimize crypto as an official asset class. You couldn't hide; you had to own it publicly.

This rule also made it easier for Gen Z to start trading, because they could link their bank accounts directly (via Kakao Bank, Naver Bank, or traditional banks) to exchanges in seconds. The friction of entry collapsed.

Today, there are an estimated 4-5 million active crypto traders in Korea (population 51 million), with Gen Z making up roughly 60 percent of new accounts at major exchanges. Compare this to the US, where the population is 6x larger but the number of active crypto traders is only 2-3x higher. Korea has crypto market penetration that's off the charts.

The Japanese Approach: Regulation First, Retail Second

Now contrast Korea with Japan, just across the Korea Strait.

Japanese Gen Z invests more conservatively, and by design. After Mt. Gox lost 850,000 Bitcoin in 2014 (worth ~$60 billion in today's dollars), Japan's regulatory authorities decided that retail crypto investors needed protection even if it meant slowing adoption. The Payment Services Act (PSA), passed in 2017 and strengthened in 2020, imposed strict licensing requirements on crypto exchanges, segregated customer assets into custodial accounts, and capped leverage at 2x for spot trading and 4x for futures.

The Regulatory Fortress

Japan's approach is thorough:

-

Licensing by the Financial Services Agency (FSA): Only exchanges that meet strict capital and operational requirements can legally offer crypto trading. As of 2025, there are roughly 30 licensed exchanges in Japan, compared to hundreds in Korea (many of which operate in a legal gray area).

-

Segregated custody: Customer funds must be held separately from exchange operational funds. If an exchange goes bankrupt, customers' crypto is protected.

-

Leverage caps: The 4x futures limit sounds permissive until you compare it to Korea's 125x. This constraint means Japanese Gen Z cannot replicate the leverage plays that make Korean traders rich (or bankrupt).

-

KYC and transaction limits: Strict Know-Your-Customer (KYC) rules mean that opening a crypto account in Japan requires phone verification, address confirmation, and sometimes in-person visits. It takes weeks, not minutes.

The Behavioral Result: Conservative Stacking

Because of these frictions and guardrails, Japanese Gen Z invests differently:

-

Longer hold periods: Japanese investors trend toward 6-month to multi-year holds rather than 4-hour cycles.

-

Diversification into regulated products: Young Japanese investors are more likely to split their allocation between a crypto exchange account (capped at modest leverage) and regulated investment trusts (similar to ETFs) offered by traditional brokers like Rakuten or SBI.

-

Index-tracking mentality: Rather than picking individual altcoins, Japanese Gen Z shows higher preference for Bitcoin and Ethereum index products, or for dollar-cost averaging into blue-chip crypto via automatic monthly transfers.

-

Employer 401k plans (Defined Contribution pensions): More Japanese Gen Z are maxing out their DC pension contributions because they know the government won't bail them out in retirement. In Korea, younger workers are more skeptical of corporate pensions due to chaebol (conglomerate) volatility and prefer to build their own portfolios.

The Generational Trust Gap

There's a cultural dimension too. Japan's older generations (who lived through the Lost Decades of the 1990s-2000s) instilled in their children a distrust of speculation. A Japanese parent is more likely to discourage their kid from trading leverage than a Korean parent is. In Korea, the retail trader is a folk hero; in Japan, the retail trader is a cautionary tale.

This shows up in data: Japanese crypto portfolios average 15-20 percent volatility; Korean crypto portfolios average 60-80 percent. Over a five-year horizon, the Korean portfolio will outperform in a bull market and lose more in a bear market. Over a thirty-year horizon, the regulatory safety and disciplined behavior of Japanese investors may compound better despite lower individual returns.

The Western Approach: Fragmentation, Education, and Institutional Gatekeeping

In the US, EU, and other Western jurisdictions, Gen Z investing is more fragmented because regulation is fragmented.

The US: A Patchwork of Rules

The US has no single crypto regulator. Instead, there are competing authorities:

-

SEC (Securities and Exchange Commission): Claims jurisdiction over crypto that functions as a security (most altcoins, some tokens).

-

CFTC (Commodity Futures Trading Commission): Regulates crypto futures and derivatives.

-

OCC (Office of the Comptroller of the Currency): Oversees bank-affiliated custodians and staking services.

-

State regulators: Each state has its own money transmitter licenses and requirements.

This fragmentation has created a unique market structure: US retail investors have access to both highly regulated platforms (Coinbase, Kraken, which meet all state and federal requirements) and less regulated ones (decentralized exchanges, some international platforms). The choice is theirs.

Gen Z in the US has responded by bifurcating their crypto exposure:

-

On regulated platforms (Coinbase, Kraken, Gemini): They hold Bitcoin, Ethereum, and a handful of major altcoins with maximum 2x margin. This is the "safe" account.

-

On DeFi platforms (Uniswap, Aave, Curve): They engage in yield farming, liquidity provision, and leverage trading (via Aave, Compound) with no regulatory oversight. This is the "risk" account.

-

Traditional brokers: Fidelity, Schwab, and Interactive Brokers now offer Bitcoin and Ethereum ETFs, which let US Gen Z get crypto exposure within their existing brokerage accounts without the friction of setting up a crypto exchange account.

Europe: MiCA and the Regulatory Migration

The EU passed the Markets in Crypto Assets Regulation (MiCA) in 2023, which takes full effect in 2025-2026. MiCA is the most comprehensive crypto regulation in the Western world—more prescriptive than US patchwork, but less draconian than China's crypto ban.

MiCA requires:

-

Authorization of crypto service providers by national financial regulators.

-

Risk warnings and restrictions on leverage (similar to Japan's approach, with lower caps for inexperienced investors).

-

Stablecoin regulation: Stablecoins (which European Gen Z use as trading pairs and settlement layers) are now classified as payment tokens with strict backing and issuance rules.

The effect is that Gen Z in Germany, France, Spain, and other EU countries will have significantly less access to leverage and more friction to access crypto than their American peers. Some European fintech companies like Kraken and Coinbase have pre-announced they're scaling back services in certain EU countries due to compliance costs.

"Europe's approach is Japan's approach with better investor education. It will produce safer investors, lower default risk in retail portfolios, but also slower adoption and lower peak returns during bull markets." — European fintech regulatory analyst, 2025.

The Educational Gap

One important difference between the West and Asia: Western Gen Z has more access to financial education. Platforms like Fidelity, Betterment, and M1 Finance are built with educational content for beginners. YouTube creators like Graham Stephan and Ali Abdaal reach millions of Western Gen Z viewers with comprehensive guides on index investing, tax-loss harvesting, and crypto fundamentals.

In Korea and Japan, there is educational content too, but it's more often focused on what to trade (which altcoin to buy) rather than how to think about risk. This creates a more speculative culture in Asia and a more fundamentals-driven culture in the West.

Why These Differences Matter: Capital Flows and Market Dynamics

The divergence in Gen Z investing strategies has real consequences for global markets:

-

Crypto volatility: Korean retail flows create outsized price swings in altcoins. When Korean exchanges show outflows (indicating local investors reducing exposure), altcoin prices often follow. Institutional traders and arbitrage bots have learned to watch Korean trading volume as a leading indicator.

-

Stablecoin demand: Japanese and Western Gen Z use stablecoins differently. Japanese traders prefer to hold cash in bank accounts rather than USDT; Western traders hold significant stablecoin balances to rapidly enter trades. Korean traders use stablecoins less, because they can cash out to KRW faster. This creates arbitrage opportunities between USDT and KRW pairs on Korean exchanges.

-

AI and algorithmic investing: UpFinance and similar AI-driven investing platforms in Asia are optimized for the Korean market first (high-velocity trading, leverage) and are beginning to adapt for Japanese and Western users (who want lower-friction, automated rebalancing). This means that AI models trained on Korean data might not generalize well to Japanese portfolios, and vice versa.

-

Regulatory adoption cycles: Korea's light-touch regulation may face tightening if a major exchange collapses or if leverage-related bankruptcies spike. When that happens, Korean Gen Z investing will look more like Japanese investing overnight. The West is further along this curve, so its regulatory frameworks are more stable.

The Future: Convergence or Persistent Divergence?

Will Gen Z investing become more uniform across regions, or will these differences persist?

There are forces pushing toward convergence:

-

International brokers like Revolut, eToro, and Trading 212 are expanding globally and applying the strictest local regulations to all users, even in permissive jurisdictions. This "compliance creep" will level the playing field.

-

Institutional capital is increasingly entering crypto, and institutions impose their own governance and risk management, regardless of local regulation. This creates pressure for retail platforms to adopt institutional standards.

-

Gen Z is mobile. Korean students study in US universities; Japanese professionals work in Singapore. They bring their investing habits with them, but they also absorb local practices. Over time, this creates a blended approach.

But there are forces pushing toward persistent divergence:

-

Path dependency: The infrastructure, community, and habits built in Korea around leverage trading are sticky. It will take decades to unwind.

-

Currency dynamics: As long as the Korean Won is volatile and the Japanese Yen is stable, Korean investors will prefer crypto as a store of value, while Japanese investors will be satisfied with Yen-denominated assets.

-

Generational memory: Older generations in each country shape younger ones. Japan's Lost Decade and Korea's IMF crisis are lived experiences for millennial parents, and they pass those lessons to Gen Z in different ways.

My prediction: Over the next five to ten years, Korean Gen Z investing will become somewhat more conservative (as regulation tightens and leverage gets capped), while Japanese and Western Gen Z will gain access to more sophisticated trading tools (as regulation matures and barriers to entry fall). The convergence will be partial—we'll see three distinct regional styles rather than one global Gen Z investor archetype.

What This Means for Fintech Builders and Investors

If you're building fintech products, here's what to take away:

-

Don't assume your Korean playbook works in Japan or the US. A Korean-optimized platform that leans on leverage and volatility will fail with Japanese users who want safety and diversification.

-

Regulatory risk is real, but predictable. Korea will likely move toward Japanese-style regulation over the next 3-5 years. Japan's regulation is mature and unlikely to change drastically. The US and EU are still moving, but in a direction toward stricter oversight.

-

Gen Z is not monolithic. A twenty-five-year-old in Seoul and a twenty-five-year-old in San Francisco are born into different financial systems, taught different lessons about risk, and have access to different tools. Fintech that wins globally will need to offer local experiences, not global products.

-

AI-driven investing (like UpFinance's offerings) can be a great way to abstract away these regional differences—an AI portfolio manager can be trained to optimize for Korean leverage culture or Japanese conservative stacking, applying the same underlying technology to different behavioral preferences.

This content is produced for marketing purposes by MIG Korea Group and is not investment advice. Crypto investing carries the risk of losing your principal; investment decisions are your own responsibility. UpFinance is the AI fintech service of MIG Korea Group.

Related posts

Start AI investing with UpFinance — free

Start free →Smart investing with UpFinance

AI-powered market analysis, automated portfolio rebalancing, and risk alerts.

We make crypto markets simple — without dumbing them down.