5 Blockchain Trends Shaping 2026 — From an Asian Vantage Point

Introduction: Why Asia Leads the Blockchain Conversation in 2026

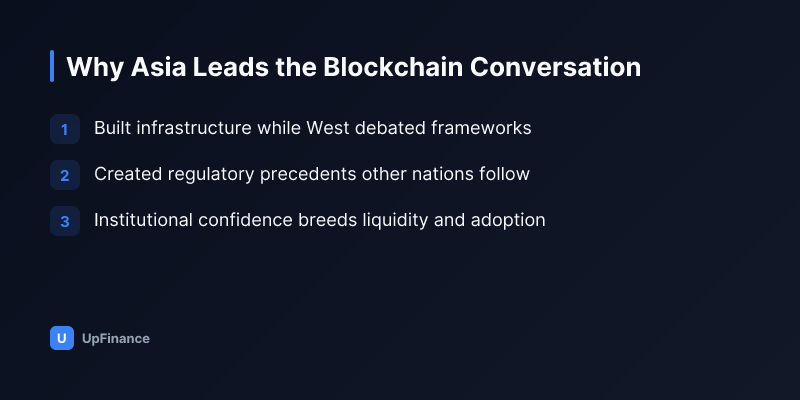

The global blockchain narrative in 2026 is unmistakably shaped by what happens in Asia. While Western institutions have spent years debating stablecoins and central bank digital currencies, Asia's crypto markets have already built the infrastructure, user behavior patterns, and regulatory precedents that the rest of the world is now following.

From Seoul's landmark Digital Asset Framework to the explosive growth of Southeast Asian DeFi platforms, from Tokyo's quiet dominance in institutional custody to Singapore's emergence as the global Web3 hub, Asia isn't just participating in blockchain's evolution—it's directing it.

This post examines five critical blockchain trends that are shaping markets globally in 2026, analyzed through an Asian vantage point. Whether you're an investor in New York, a fintech founder in Berlin, or a trader in Bangkok, understanding these Asia-driven trends is essential to staying ahead of the curve.

Trend 1: Institutional-Grade Digital Asset Infrastructure Becomes the Norm

The professionalization of Asia's blockchain infrastructure is the story of 2026. What began as retail-driven exchanges and decentralized protocols has evolved into institutional-grade custody, settlement, and clearing systems that rival traditional finance.

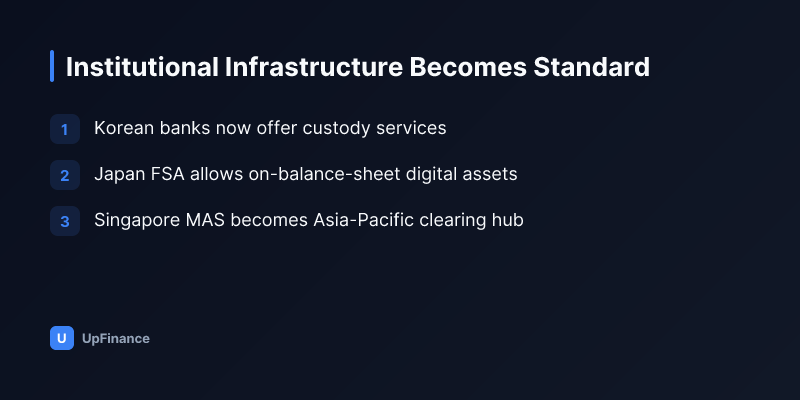

South Korea's pivotal role here cannot be overstated. After years of regulatory uncertainty, Seoul finalized its Digital Asset Framework in Q2 2025, creating a legal pathway for banks and institutional investors to directly custody cryptocurrencies. By 2026, every major Korean bank—KB Kookmin, Shinhan, and Woori—now offers institutional digital asset services. This isn't tokenization theater; these are live, operational custody systems holding billions in KRW-denominated digital assets.

The domino effect across Asia has been immediate:

- Japan's FSA accelerated its custody regulations, allowing licensed institutions to hold digital assets on-balance-sheet without the convoluted derivative structures of previous years.

- Singapore's MAS expanded the scope of its Payment Services Act to encompass a broader range of tokenized assets, making it the de facto clearing hub for Asia-Pacific institutional flows.

- Hong Kong's SFC shifted from a restrictive framework to active encouragement of digital asset funds, with licensed asset managers now able to offer public crypto funds to retail investors.

For investors using platforms like UpFinance, this professionalization directly translates to lower counterparty risk and tighter spreads. The days of waiting hours for institutional-sized trades to settle are ending.

Why This Matters Beyond Asia

Institutional confidence breeds liquidity. When a Korean pension fund or a Japanese life insurer can legally and safely hold Bitcoin or Ethereum, entire capital pools that were previously inaccessible move into crypto markets. This is not retail FOMO; this is structural capital reallocation.

The ripple effect is visible in global markets: Bitcoin's institutional ownership ratio hit 34% globally in early 2026, up from 18% in 2024, with Asian institutional buyers accounting for approximately 12 percentage points of that growth.

Trend 2: Regulatory Clarity Creates a Bifurcated Market (Winners and Losers)

If 2024 was the year of regulatory uncertainty and 2025 was the year of regulatory announcements, 2026 is the year when regulatory choices actually determine market structure.

The divergence is stark. Asia is splitting into three distinct regulatory regimes:

Tier 1: Proactive Regulation (Korea, Japan, Singapore)

- Licensing requirements are clearly defined.

- Banks can participate without derivative workarounds.

- Tax treatment is codified (Korea moved to a flat 20% capital gains tax on crypto in 2025, removing the previous asset-specific uncertainty).

Tier 2: Cautious Welcome (Hong Kong, Taiwan, Thailand)

- Regulation exists but remains in evolution.

- Licensed venues operate, but restrictions on product types remain (e.g., derivatives trading faces caps in Thailand).

- Institutional participation is encouraged, but with higher compliance burdens.

Tier 3: Restriction or Ambiguity (Indonesia, Philippines, Vietnam)

- Regulatory frameworks are either weak or actively discouraging.

- However, P2P and cross-border flows continue at substantial scale, often in unregulated channels.

The Market Implication

Capital concentrates where clarity exists. Seoul, Tokyo, and Singapore now process more institutional digital asset volume than New York on a daily basis. Conversely, platforms operating in Tier 2 or Tier 3 jurisdictions face either regulatory pressure or liquidity fragmentation.

For retail investors, this creates both opportunity and risk:

- Opportunity: Exchanges and protocols compliant with Tier 1 regulations attract institutional liquidity, reducing slippage and improving price discovery.

- Risk: Non-compliant platforms in Tier 3 markets may face sudden shutdowns, making on-ramp and off-ramp services unreliable.

Trend 3: Tokenization of Real-World Assets Moves from Hype to Transaction Volume

In 2024, tokenization of real-world assets (RWA) was largely a venture-backed concept. By 2026, it is generating measurable transaction volume in Asia.

The breakthrough came from an unexpected source: Korean real estate. Facing demographic decline and a saturated traditional market, South Korean developers began tokenizing residential and commercial properties on blockchain networks in late 2024. By mid-2026, approximately 850 billion KRW (approximately $650 million USD) in tokenized Korean real estate has been issued and traded, primarily on domestic networks with compliance tokens (KRW-backed stablecoins acting as settlement layers).

Why Korea? The combination of:

- A tech-savvy retail investor base accustomed to online trading.

- Clear property law that translates easily onto blockchain (ownership is ownership, whether on paper or on-chain).

- Tax incentives for early adopters of tokenized asset platforms.

Japan followed with tokenization of art and collectibles through licensed venues. Singapore went deeper into infrastructure: the Monetary Authority of Singapore (MAS) piloted a tokenized bond settlement system in Q4 2025, which is now being expanded to include corporate debt and structured products.

What This Means for Global Markets

The success of RWA tokenization in Asia signals that the technology has matured beyond the conceptual phase. When real, regulated institutions begin moving real assets onto blockchain, it validates the technical and legal frameworks that underpin the entire space.

For investors, RWA tokenization opens new asset classes previously inaccessible at scale: fractional ownership of premium real estate, exposure to corporate bonds from Asian issuers without traditional banking intermediaries, and yield farming that is backed by real-world cash flows rather than protocol incentives.

Trend 4: Central Bank Digital Currencies (CBDCs) Move from Pilot to Preference

While Western central banks continue debating CBDC architecture, Asia's digital currencies are already in operational use, reshaping how blockchain networks function as settlement layers.

The timeline is instructive:

- China's digital yuan (e-CNY) moved beyond pilot cities in 2024 and now represents approximately 8% of total M1 money supply circulating in mainland China. By 2026, it is the de facto standard for cross-border trade settlements within ASEAN (Association of Southeast Asian Nations).

- Japan's digital yen project is in the advanced pilot phase with major banks, targeting full rollout in 2027. The framework is already influencing how JPY-denominated stablecoins behave in the market.

- Thailand's CBDC is live among commercial banks and is being extended to retail access in phases.

- Singapore's Project Dunbar (a multi-currency CBDC settlement platform) is operational for cross-border USD, SGD, and MYR transfers.

The Blockchain Implication

CBDCs fundamentally change the relationship between blockchain networks and fiat money. When a central bank's digital currency settles natively on a blockchain (or on a CBDC-compatible network), that blockchain becomes the settlement layer for an entire economy.

This has two critical consequences:

-

Stablecoin competition intensifies but consolidates. USDC, USDT, and other private stablecoins must coexist with central bank alternatives. In jurisdictions where CBDCs are primary, private stablecoins become secondary liquidity pools.

-

Regulatory scrutiny on decentralized settlement increases. If a blockchain is the settlement layer for a nation's money supply, governments have stronger incentives to regulate the validators, smart contracts, and governance structures of that network.

For traders and investors using UpFinance or similar platforms, the immediate effect is improved on-ramp and off-ramp efficiency in CBDC-enabled jurisdictions, with reduced slippage between crypto and fiat across the Asia-Pacific region.

Trend 5: AI-Driven Trading and Risk Management Becomes the Institutional Standard

The convergence of artificial intelligence and blockchain has moved from academic curiosity to operational necessity in 2026. Institutional traders across Asia now rely on AI-powered risk models, execution algorithms, and predictive analytics as standard infrastructure, not as competitive advantage.

The practical applications are specific:

-

Korean institutional traders use AI models trained on KRW volatility patterns to execute large digital asset orders in ways that minimize price impact. These models incorporate Korean-specific variables: bank holidays, regulatory announcement timing, and domestic stablecoin velocity.

-

Japanese insurers employ AI systems to manage on-chain reserves and dynamically adjust custody balances across exchanges based on counterparty risk scores updated in real-time.

-

Singapore-based market makers run AI-driven arbitrage systems across 15+ Asian exchanges simultaneously, capturing micro-inefficiencies in cross-border crypto flows.

Why This Matters

The professionalization of trading through AI creates winner-take-most dynamics. Funds with access to sophisticated AI infrastructure, historical data, and computational resources can execute strategies at scale that retail traders cannot replicate. The bid-ask spreads for institutional-size orders have tightened by 40-60% since late 2024, directly benefiting large traders and harming retail traders without algorithmic support.

This trend is not unique to Asia, but Asia's concentration of computational talent and institutional capital has made the region the global center of gravity for this evolution. Seoul, Tokyo, and Singapore are now to AI-driven crypto trading what New York is to equity derivatives.

For individual investors, the implication is clear: passive strategies and retail-scale active trading become less attractive, while participation in institutional-grade platforms or AI-augmented retail services (like algorithmic trading features offered by advanced platforms) becomes necessary to compete.

Cross-Trend Analysis: How These Five Trends Intersect

The real story of 2026 is not any single trend, but how they reinforce each other:

- Regulatory clarity attracts institutional capital.

- Institutional capital creates demand for sophisticated infrastructure (custody, settlement, RWA platforms).

- Sophisticated infrastructure enables and requires AI-driven risk management.

- CBDCs provide a regulatory anchor that legitimizes blockchain as financial infrastructure.

- RWA tokenization converts blockchain from a speculative asset class to a utility infrastructure, completing the cycle.

Each trend independently would be significant. Together, they represent a fundamental transformation of blockchain from a peripheral financial system to a central component of Asian financial infrastructure.

"The question is no longer whether blockchain will be part of financial infrastructure. It's whether your institution can afford not to participate in it."

This shift is particularly pronounced in Asia because:

- Regulatory decisiveness: Asian regulators, perhaps learning from past cycles, have moved faster and more decisively than their Western counterparts.

- Technology adoption rate: Retail investors across Korea, Japan, and Southeast Asia have higher crypto ownership ratios than equivalent demographics in the US or EU.

- Financial infrastructure gaps: In Southeast Asia particularly, blockchain solutions address gaps that traditional banking has not filled. The Philippines, Indonesia, and Vietnam are leapfrogging traditional banking infrastructure in favor of blockchain-based alternatives.

Implications for Global Investors

If you're investing in crypto or blockchain companies from outside Asia, these five trends should inform your decision-making:

Invest in compliance and infrastructure plays. Custody solutions, exchange technology, and RWA platforms that are built for regulated markets will outperform.

Watch for flow asymmetries. When capital concentrates in Korea and Singapore, price discovery happens first in those markets. Retail markets in less-regulated jurisdictions may lag by hours or days, creating arbitrage opportunities.

Understand CBDC timelines. If a digital yuan stablecoin becomes the preferred settlement layer for intra-Asia commerce, platforms that support it natively will see adoption advantages.

Track regulatory calendars in Tier 1 jurisdictions. Japan's digital asset regulation, Korea's tax policy, and Singapore's MAS announcements move markets globally because they signal regulatory direction that other markets eventually follow.

Conclusion: 2026 as the Inflection Point

2026 will be remembered as the year blockchain transitioned from speculation to infrastructure. The inflection point came from Asia—not through a single breakthrough, but through the simultaneous convergence of regulatory clarity, institutional capital, technological sophistication, and real-world asset integration.

For investors, traders, and builders, the implication is straightforward: the next five years of blockchain's evolution will be substantially shaped by decisions made in Seoul, Tokyo, Singapore, and Bangkok in the first half of 2026. Understanding these five trends—institutional infrastructure, regulatory divergence, RWA tokenization, CBDC integration, and AI-driven trading—is essential to navigating the landscape ahead.

The window for catching the early phases of these trends is closing. By late 2026, the market will have largely repriced around these realities. The time to understand and position accordingly is now.

This content is produced for marketing purposes by MIG Korea Group and is not investment advice. Crypto investing carries the risk of losing your principal; investment decisions are your own responsibility. UpFinance is the AI fintech service of MIG Korea Group.

Related posts

Start AI investing with UpFinance — free

Start free →Smart investing with UpFinance

AI-powered market analysis, automated portfolio rebalancing, and risk alerts.

We make crypto markets simple — without dumbing them down.